Product Pricing

Unit 1: Market - Meaning and Types

1.1 Definition of Market

A market is an arrangement where buyers and sellers exchange goods and services at an agreed price.

1.2 Types of Markets

A. Based on Geographical Area:

TypeMeaningExampleLocal MarketLimited to a small area, perishable goodsVegetables, milk, fishNational MarketWithin one country, transportable goodsRice, wheat, clothesInternational MarketAcross countries, valuable goodsTea, coffee, machinery

B. Based on Commodities:

TypeMeaningExampleCommodity MarketGoods marketRice market, cloth marketFactor MarketFactors of production marketLabour market, capital market

C. Based on Time:

TypeMeaningVery Short PeriodSupply fixed (daily market)Short PeriodCan adjust some factorsLong PeriodCan adjust all factors

Unit 2: Perfect Competition Market

2.1 Definition

Perfect Competition is a market structure with:

- Many buyers and sellers

- Homogeneous products

- Free entry and exit

- Perfect information

- Price takers (firms accept market price)

2.2 Characteristics

- Large number of buyers/sellers – No single firm affects price

- Homogeneous product – Identical goods from all sellers

- Free entry and exit – No barriers

- Perfect knowledge – All know prices and quality

- Perfect mobility – Factors move freely

- No government intervention – Price determined by demand-supply

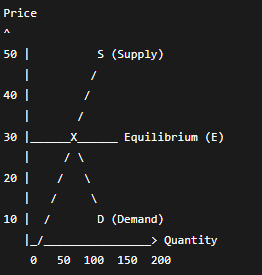

2.3 Price Determination in Perfect Competition

Price is determined where market demand = market supply.

Table: Demand-Supply Schedule

Price (Rs.)Quantity DemandedQuantity SuppliedMarket Condition1020050Shortage (Excess Demand)20150100Shortage30100100Equilibrium4050150Surplus (Excess Supply)5025200Surplus

Diagram:

text

Equilibrium Price: Rs. 30

Equilibrium Quantity: 100 units

E = Equilibrium point (Demand = Supply)

Unit 3: Monopoly Market

3.1 Definition

Monopoly is a market structure with:

- Single seller

- No close substitutes

- Barriers to entry

- Price maker (sets own price)

3.2 Characteristics

- Single seller – Only one firm controls market

- No close substitutes – Unique product

- Barriers to entry – Others cannot enter

- Price maker – Sets price to maximize profit

- Downward sloping demand curve – Must lower price to sell more

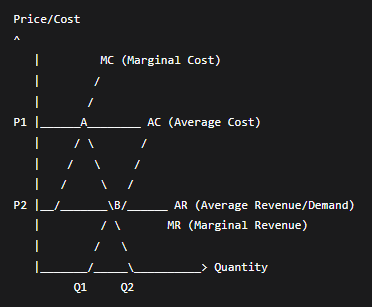

3.3 Price Determination in Monopoly

Monopolist sets price where MR = MC (Marginal Revenue = Marginal Cost).

Diagram:

Equilibrium: Point A (MR = MC)

Price: P1 (from demand curve)

Quantity: Q1

Profit: Area (P1-AC at Q1) × Q1

Unit 4: Comparison of Markets

4.1 Perfect Competition vs Monopoly

BasisPerfect CompetitionMonopolyNumber of sellersManyOneProductHomogeneousUniqueEntry/ExitFreeRestrictedPrice controlPrice takerPrice makerDemand curveHorizontal (elastic)Downward slopingProfitNormal in long runCan be supernormalEfficiencyMore efficientLess efficient

4.2 Real World Examples

Perfect Competition:

Agricultural markets (rice, wheat)

Stock exchange

Monopoly:

Nepal Electricity Authority (NEA)

Nepal Oil Corporation (NOC)

Patented medicines

Key Terms & Definitions

Market: Place/arrangement for buying-selling.

Equilibrium Price: Price where demand = supply.

Price Taker: Firm accepting market price (perfect competition).

Price Maker: Firm setting own price (monopoly).

Homogeneous Product: Identical goods from all sellers.

Barriers to Entry: Obstacles preventing new firms.

MR = MC Rule: Profit maximization condition.

Important Formulas

Total Revenue (TR): Price × Quantity

Average Revenue (AR): TR ÷ Quantity = Price

Marginal Revenue (MR): ΔTR ÷ ΔQ

Profit: TR - TC (Total Revenue - Total Cost)