This chapter explains government finance - how governments collect revenue (taxes, fees) and make expenditures (public services, development). We study different types of taxes, government budgets, and how public finance affects economic development and social welfare.

Unit 1: Meaning of Public Finance

1.1 Definition

Public Finance is the study of government revenue and expenditure. It examines:

- How government collects money (taxes, fees, etc.)

- How government spends money (public services, development)

- How government manages public debt

- How government budget is prepared

According to Adam Smith:

"Public finance is an inquiry into the nature and principles of the state's revenue and expenditure."

Unit 2: Government Expenditure

2.1 Definition

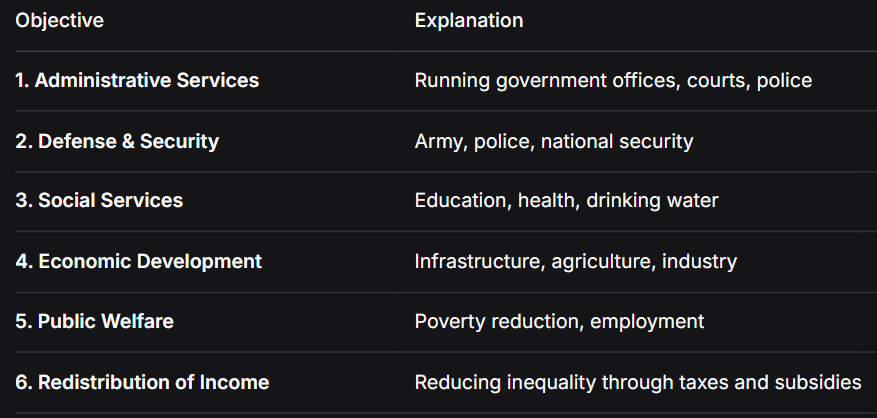

Government Expenditure refers to money spent by government for:

- Public administration

- Defense and security

- Social services (education, health)

- Economic development

- Public welfare

2.2 Importance/Objectives of Government Expenditure

Unit 3: Classification of Government Expenditure

3.1 Types of Government Expenditure in Nepal

A. Regular/Recurrent Expenditure:

- Day-to-day government operations

- Examples: Salaries, office expenses, maintenance

B. Capital/Development Expenditure:

- Long-term development projects

- Examples: Road construction, building schools, irrigation projects

C. Financial Management:

- Public debt management

- Examples: Loan repayment, interest payments

3.2 Major Heads of Expenditure in Nepal:

- Administrative Services → Government offices

- Economic Services → Agriculture, industry, tourism

- Social Services → Education, health, water supply

- Defense → Army, police

- Public Debt → Loan repayment

Unit 4: Government Revenue

4.1 Definition

Government Revenue is money received by government from various sources.

4.2 Sources of Government Revenue

A. Tax Revenue:

- Income Tax → Tax on individual/company income

- Value Added Tax (VAT) → Tax on value addition

- Custom Duty → Tax on imports/exports

- Excise Duty → Tax on production of goods

- Land Revenue → Tax on land/property

B. Non-Tax Revenue:

- Fees → For specific services (license fees)

- Fines → Penalties for breaking laws

- Royalty → From natural resources

- Dividends → From public enterprises

- Foreign Grants → Aid from other countries

C. Foreign Loans and Grants:

- Loans from World Bank, ADB, etc.

- Grants from foreign governments

Unit 5: Taxes

5.1 Definition of Tax

Tax is a compulsory payment to government without direct benefit to taxpayer.

Characteristics of Tax:

- Compulsory payment

- No direct benefit

- Used for public welfare

- Legal payment

5.2 Types of Taxes

A. Direct Taxes:

- Taxpayer cannot shift burden to others

- Examples: Income tax, property tax, wealth tax

B. Indirect Taxes:

- Taxpayer can shift burden to consumers

- Examples: VAT, sales tax, custom duty

Comparison:

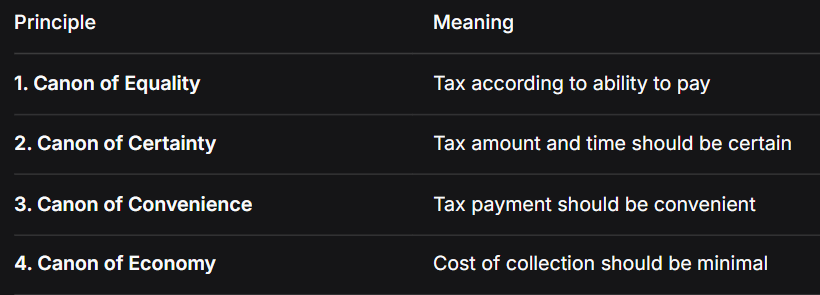

5.3 Principles/Canons of Taxation (Adam Smith)

5.4 Tax Systems

1. Progressive Tax:

- Tax rate increases as income increases

- Example: Income tax in Nepal

- Advantages: Reduces inequality, based on ability to pay

- Disadvantages: Discourages saving and investment

2. Proportional Tax:

- Same tax rate for all income levels

- Example: 10% tax for everyone

- Advantages: Simple to calculate

- Disadvantages: Unfair to poor people

3. Regressive Tax:

- Tax rate decreases as income increases

- Example: Sales tax (poor pay higher percentage)

- Disadvantages: Increases inequality

- Examples in Nepal:

- Progressive: Income tax

- Proportional: Some fees

- Regressive: VAT (affects poor more)

Unit 6: Government Budget

6.1 Definition

Government Budget is an annual financial statement showing:

- Estimated revenue (income)

- Proposed expenditure (spending)

- For a financial year (Shrawan-Ashad in Nepal)

6.2 Types of Budget

A. Balanced Budget:

- Revenue = Expenditure

- Advantage: No debt

- Disadvantage: Limited development

B. Surplus Budget:

- Revenue > Expenditure

- Advantage: Savings for future

- Disadvantage: May indicate overtaxation

C. Deficit Budget:

- Expenditure > Revenue

- Advantage: More development spending

- Disadvantage: Increases debt

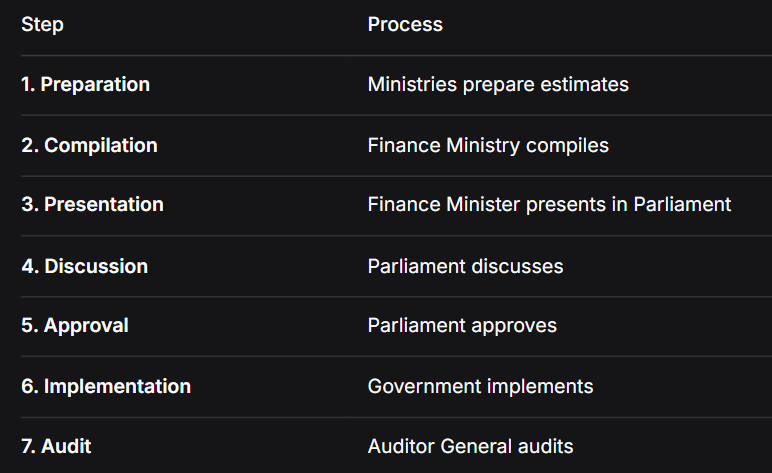

6.3 Budget Process in Nepal

Nepal's Fiscal Year: Shrawan 1 to Ashad 31 (Mid-July to Mid-July)

6.4 Components of Budget

A. Revenue Budget:

- Tax revenue

- Non-tax revenue

B. Expenditure Budget:

- Regular expenditure

- Capital expenditure

- Financial management

C. Other Components:

- Economic survey

- Policy statements

- Tax proposals

Key Terms & Definitions

- Public Finance: Study of government revenue and expenditure

- Tax: Compulsory payment to government

- Direct Tax: Tax paid directly by taxpayer (income tax)

- Indirect Tax: Tax collected through goods/services (VAT)

- Progressive Tax: Tax rate increases with income

- Budget: Government's annual financial plan

- Fiscal Year: Government's accounting year (Shrawan-Ashad in Nepal)

- Deficit Budget: Expenditure exceeds revenue

- Surplus Budget: Revenue exceeds expenditure

- Balanced Budget: Revenue equals expenditure

Important Formulas

- Tax Amount = Income × Tax Rate

- VAT Amount = Price × VAT Rate

- Budget Deficit = Total Expenditure - Total Revenue

- Budget Surplus = Total Revenue - Total Expenditure

Examples from Nepal

Major Taxes in Nepal:

Income Tax → Progressive tax system

Value Added Tax (VAT) → 13% on most goods

Custom Duty → On imports

Excise Duty → On alcohol, tobacco

Land Tax → On property

Major Expenditure Heads in Nepal:

- Education (largest share)

- Health

- Infrastructure

- Defense

- Social security